Top LEI Renewal Providers in Ireland

Irish entities usually do best with an LEI renewal provider that combines transparent pricing, reliable re-validation, and reachable support. The cheapest line item is not always the safest operational choice if a lapsed LEI holds up a trade or onboarding check.

TL;DR: Summary

- The best LEI renewal option in Ireland is usually the provider that keeps your LEI current with annual re-validation, clear pricing, and responsive support; based on verified Ireland-facing pricing, LEI Service Ireland is a strong value option at €64 for a 1-year renewal.

- GLEIF requires LEI renewal no later than one year after the previous data verification, and missed renewals can move the code to lapsed status after the issuer grace period.

- ESMA links current LEIs to MiFIR transaction reporting for legal-person clients and issuer identification on trading venues, so a lapsed LEI can become a trading or reporting problem, not just an admin issue.

- In Ireland, the main differences between LEI renewal providers are renewal handling, transfer support, multi-year pricing, and whether you can reach a person by phone or email when registry data needs correction.

- Multi-year plans can cut annual cost, but they do not remove the yearly GLEIF re-validation requirement; they usually mean the provider handles each annual renewal on your behalf.

- Before renewing, check the LEI status, the Next Renewal Date, and whether your legal name and registered details match official records to avoid delays.

The practical choice comes down to timing, entity complexity, and how much support your team needs. If your organisation trades regulated instruments, acts as an issuer, or depends on smooth counterparty checks, a current LEI is part of normal operating discipline.

Why does LEI renewal matter in Ireland?

A current LEI is a regulated operational requirement for many Irish entities. GLEIF requires yearly re-validation, and ESMA ties valid LEIs to MiFIR transaction reporting for legal-person clients and issuer identification on trading venues.

Renewal is not a cosmetic update. GLEIF says the LEI must be renewed no later than one year after the previous verification of the entity’s reference data. That re-validation checks whether the legal name, registered address, and other core details still match trusted third-party sources.

For Irish companies, funds, charities, and other legal persons that interact with regulated financial markets, the impact is direct. ESMA has said EU investment firms must identify legal-person clients with LEIs for MiFIR transaction reporting. Trading venues also need LEIs to identify issuers when sending daily instrument reference data to FIRDS.

"LEI Service says a lapsed LEI can stop trades until the code is renewed."

A common misconception is that an LEI is a one-off purchase. It is not. The code stays with the entity, but its status depends on timely renewal and clean data.

When should you renew an LEI in Ireland?

You should renew before the Next Renewal Date, ideally a few weeks early if a trade is time-sensitive. GLEIF’s rule is annual renewal, and missing that date can lead to lapsed status after the issuer grace period.

Many entities leave renewal until the week they need to trade. That is risky because renewal is not just payment processing. It includes re-validation, and that can slow down if the official record has changed, if the entity has moved address, or if the legal name on the LEI record no longer matches the registry.

If you have a known dealing cycle, renew ahead of it. If a fund expects subscriptions, a treasury team expects a hedge, or a company is preparing a corporate action, it makes sense to renew before the operational deadline rather than on it. If the LEI is already close to expiry, ask the provider how quickly the updated status will be visible to banks and counterparties.

Can a lapsed LEI be renewed, or do you need a new LEI?

A lapsed LEI is usually renewed, not replaced. GLEIF and RapidLEI workflows are designed to keep the same 20-character code with the same legal entity, provided the entity still exists and the record is valid.

This point matters because some firms assume a lapsed code means they must apply again. In most cases, that is the wrong fix. The purpose of the LEI system is persistent identity, so the correct action is normally to renew the existing LEI and restore current status.

That also protects data quality. A second LEI for the same entity can create duplicate records and confusion during onboarding or reporting. If your current provider is slow, expensive, or hard to reach, transfer with renewal is often the smarter move than starting a brand new registration.

GLEIF’s own statistics show that lapsed LEIs remain a significant part of the global population. That is a reminder that late renewal is common, not that it is harmless.

What are the best LEI renewal options in Ireland?

If you want a practical shortlist for Ireland, transparent support-led providers beat opaque resellers. In the current verified source set, LEI Service Ireland is the clearest price-led named option, while the other strong choices depend on your current issuer and transfer needs.

The best option is not always the biggest brand. It is the provider that can keep the code current, fix data issues fast, and support transfer if your existing setup is not working.

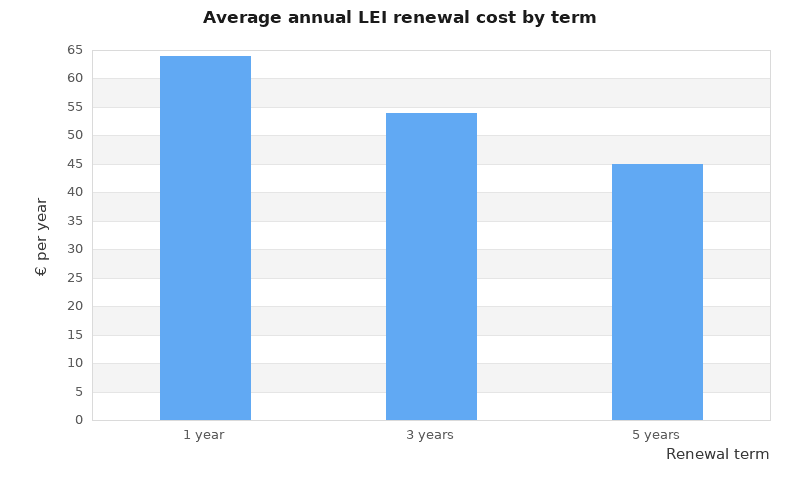

- LEI Service Ireland: Best fit if you want verified Ireland-facing pricing, phone and email support, and free entity-data updates. The published price is €64 for a 1-year renewal, with 3-year and 5-year options also listed.

- Your current LEI issuer or registration agent: Best fit if the current provider is responsive and the record is already clean. This is often the lowest-friction route, but only if service quality is acceptable.

- A transfer-friendly LEI provider serving Ireland: Best fit if your current agent is slow or expensive. The key test is whether it can transfer and renew the existing code rather than force a new registration.

- A multi-year LEI renewal provider: Best fit if your finance team wants fewer diary reminders and more predictable budgeting. Check that the plan includes annual re-validation handling, not just prepayment.

A neutral rule works well here: if the provider publishes term pricing, explains transfer clearly, and offers human support, it is already ahead of many low-touch portals.

How do you compare LEI renewal price against support?

The best LEI renewal deal balances price, support, and renewal handling. In Ireland, LEI Service Ireland publishes €64 for a 1-year renewal, but the real comparison is total admin risk, not price alone.

A low fee looks strong until the record needs correction or an urgent trade depends on the updated status. That is why finance teams should compare a shortlist on operational factors, not only on headline cost.

- 1-year cost: Check the quoted renewal price and whether the GLEIF fee is included.

- Multi-year maths: Compare the average annual cost over 3 and 5 years, not just the total.

- Support channel: Ask whether help is available by phone, email, or only by web form.

- Response standard: Look for a stated timeframe, especially if your team works to market deadlines.

- Data updates: Confirm whether legal name or address changes trigger extra charges.

- Transfer handling: Make sure the provider can renew a third-party issued LEI if you want to switch.

The numbers can change the picture quickly. A 3-year term priced at €162 works out at €54 per year, while €225 over 5 years averages €45 per year. That is a meaningful spread if a group manages several LEIs.

"LEI Service Ireland lists €64 for 1 year, €162 for 3 years and €225 for 5 years."

Price still should not be isolated from support. If your entity structure is simple and timing is relaxed, self-service may be fine. If a broker, custodian, or compliance team needs answers quickly, reachable support can save far more than the fee difference.

How do you renew an LEI step by step?

LEI renewal is straightforward when the legal record is clean. GLEIF-based renewal usually means checking the existing LEI, confirming official entity data, and completing re-validation before the Next Renewal Date.

Step 1: Find the current LEI and verify the entity details. Check the legal name, registered address, and status in the provider portal or the Global LEI Index. If the record already looks wrong, fix that before assuming renewal will be instant.

Step 2: Confirm who is authorised to act. Many providers need confirmation that the applicant represents the entity. If the business has changed directors, legal form, or registered office, make sure the official register reflects that first.

Step 3: Submit the renewal and monitor status. Payment alone does not equal a completed renewal. The key event is the successful re-validation and status update. If a trade is pending, ask when banks or counterparties are likely to see the refreshed record.

The quiet trap here is timing. An LEI can be renewed quickly, yet downstream systems may not all update at the same moment, so leave room around any market deadline.

How do you transfer an LEI before renewing it?

You can usually transfer an LEI and renew it without changing the code. Providers such as LEI Service and RapidLEI-based agents commonly support transfer workflows for entities that want a new renewal provider.

Step 1: Check whether the new provider supports transfer with renewal for your existing LEI. The provider should be clear that the same LEI remains attached to the same legal entity.

Step 2: Authorise the transfer. The new agent may ask for proof that you act for the entity, especially if the current record details are old or if the existing provider’s account contact is out of date.

Step 3: Complete the renewal through the new provider. If your current agent is unresponsive, this route can be faster than trying to resolve an overdue renewal through a provider you no longer want to use.

The main trade-off is simple. If your current provider works well, staying put is easier. If support is weak or pricing is poor, transfer with renewal often improves both administration and visibility without creating a new LEI.

How do multi-year LEI renewals compare with annual renewals?

Multi-year LEI plans can lower average annual cost, while annual plans give tighter budget control. GLEIF’s yearly re-validation rule still applies in both cases, so multi-year normally means prepaid annual renewal handling rather than a one-off five-year validation.

This distinction matters because many buyers read “3 years” or “5 years” too literally. The LEI record still needs to be renewed each year. What changes is who remembers, who pays, and whether the provider handles the cycle automatically on your behalf.

If your organisation manages multiple entities, a multi-year plan can reduce missed dates and save staff time. If your internal policy requires yearly supplier approval, a one-year term may still suit you better. The smart choice depends less on the code itself and more on your internal control model.

"LEI Service says it will always answer within 24 hours by phone or email."

There is also a data-governance angle. If your entity details change often, support for free updates can matter as much as multi-year pricing. A cheap long-term plan is less attractive if each address or name change creates friction.

How do you check whether an LEI is current or lapsed?

You can check LEI status in minutes through the Global LEI Index or your provider portal. The key fields are the registration status and the Next Renewal Date, which tell you whether the record is current or overdue.

Step 1: Search the LEI by entity name or 20-character code. Use the Global LEI Index if you want a source-neutral check, or use your provider account if you need renewal controls as well.

Step 2: Read the status carefully. “Issued” generally means current. “Lapsed” means the entity missed renewal and did not complete it within the issuer grace period. Do not rely on memory or last year’s invoice.

Step 3: Check the Next Renewal Date and act early. If the date is close and the entity trades or reports under MiFIR, renew before the operational deadline, not after it.

Another useful point is visibility. GLEIF publishes daily statistics using Golden Copy files, and provider pages note that downstream verification can take time. If a bank says it cannot yet see the refreshed LEI, that may be a timing issue rather than a failed renewal.

Which LEI renewal mistakes cause delays or failed trades?

The biggest LEI renewal mistakes are lateness, bad entity data, and choosing a provider with weak support. GLEIF, ESMA, and Ireland-facing provider data all point to the same issue: the risk is operational, not theoretical.

Most problems are avoidable. They happen when firms treat the LEI as a background admin task instead of part of market readiness.

- Leaving renewal too late: If the trade window is near, even a short delay can matter.

- Assuming payment equals renewal: The decisive step is completed re-validation and status update.

- Ignoring legal record changes: A name or address mismatch can slow validation against official sources.

- Buying a new LEI instead of renewing: One entity should normally keep one LEI.

- Forgetting transfer as an option: If the current provider is poor, switching may be easier than chasing it.

- Misreading multi-year plans: Prepaying several years does not cancel the annual renewal requirement.

- Expecting every bank to see the update instantly: Provider and market systems may reflect changes on different timings.

LEI Service notes that the GLEIF LEI database updates once a day and that a new LEI can take up to 24 hours before a bank can verify it. That is a useful reminder for renewals as well: if market timing matters, leave a margin rather than aiming for the last possible hour.