Who Needs an LEI in Ireland? Companies, Funds, SPVs and Charities Explained

An LEI, or Legal Entity Identifier, is a 20 character code used to identify legal entities in financial markets and regulatory reporting. In Ireland, many organisations first hear about it when a broker, bank, fund administrator or compliance adviser asks for one urgently.

That timing often creates the wrong impression. An LEI is not required simply because an entity exists. The strongest trigger is usually regulated financial activity. A company can trade for years without one, while a newly active SPV or a charity entering a derivative contract may need an LEI straight away.

That is the key point for Irish businesses, funds, Section 110 vehicles and non-profits alike: legal form matters less than what the entity is doing, who it is dealing with, and what must be reported to regulators or trade repositories.

When an LEI is required in Ireland

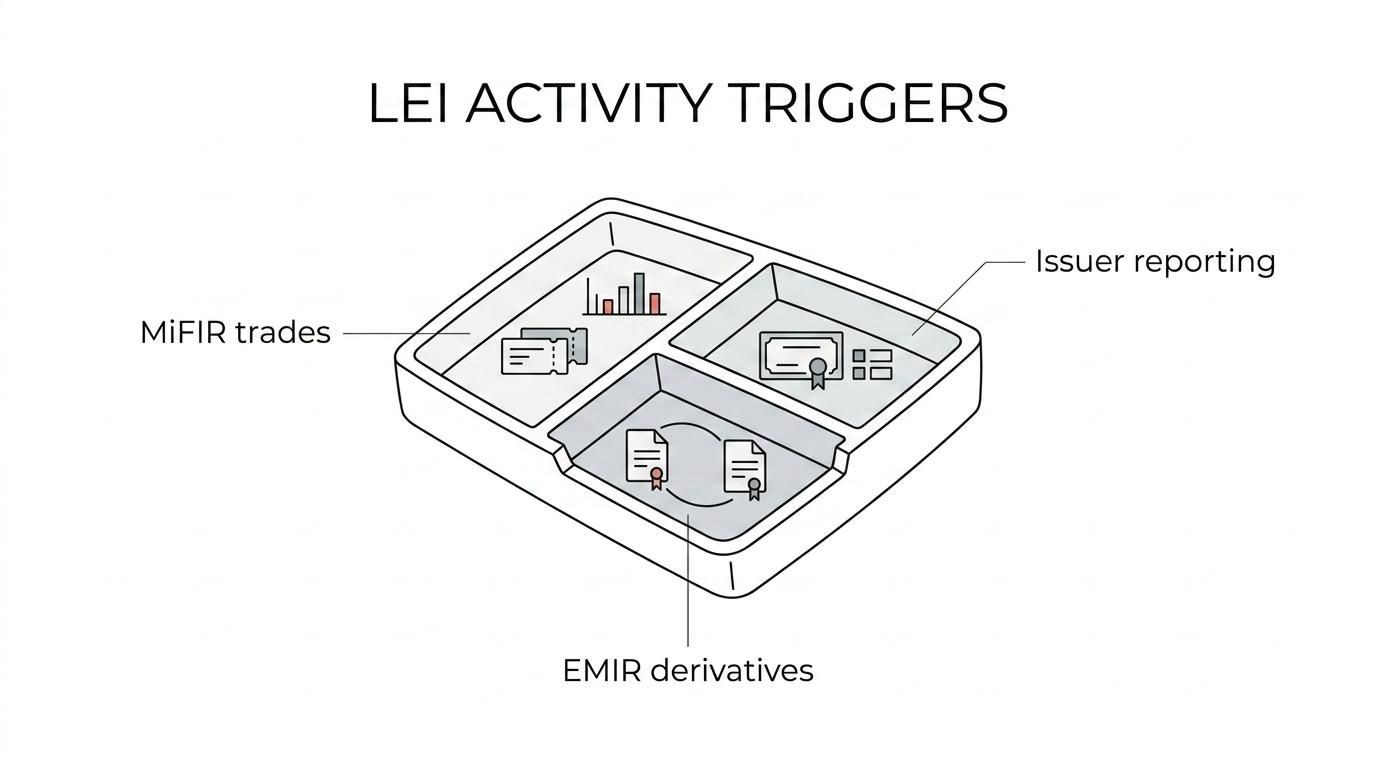

The clearest Irish and EU triggers sit inside reporting frameworks. Under MiFIR, EU investment firms must identify clients that are legal persons with LEIs for MiFID II transaction reporting. ESMA has also said that trading venues must identify each issuer of a financial instrument traded on their systems with an LEI when they make daily reference data submissions to FIRDS.

That means the LEI requirement often appears before a trade is processed, not after. If an Irish company wants to buy or sell certain financial instruments through an investment firm, the firm may not be able to complete its reporting obligations without the client’s LEI. In practice, the request can arrive at account opening, before trading, or when a new instrument is added.

EMIR creates another major trigger. For derivative contracts reported to EU trade repositories, the LEI is mandatory for legal entities involved in the reportable arrangement. ESMA’s guidance extends beyond the two counterparties and includes other entities identified in the report, depending on the structure.

| Entity type in Ireland | Common LEI trigger | Practical effect |

|---|---|---|

| Private or public company | Trading reportable financial instruments through an investment firm | LEI may be needed before the trade can be reported |

| Issuer of listed or traded instruments | Identification on trading venue systems and reference data reporting | LEI often becomes part of issuer onboarding |

| Fund or sub-fund | Market trading, derivatives, regulatory reporting, administrator workflows | LEI is commonly expected early |

| Section 110 SPV | Central Bank reporting and market transactions | LEI is frequently part of the reporting setup |

| Charity or non-profit company | Treasury investments, derivatives, listed securities, reporting obligations | LEI may be needed even without a commercial purpose |

Irish companies that need an LEI for MiFIR and EMIR

For ordinary Irish companies, the question is rarely “Are you incorporated?” and much more often “Are you entering a regulated transaction chain?” A manufacturing company with no financial market activity may never need an LEI. A property company using interest rate swaps, or a treasury vehicle buying bonds through an investment firm, is in a very different position.

MiFIR is the reason many companies are asked for an LEI by brokers and investment firms. If the client is a legal person, the investment firm needs that LEI for transaction reporting. No LEI can mean no report, and in practical terms that may mean no trade.

EMIR widens the picture. If an Irish company enters into a derivative contract, the LEI requirement can apply even where the company does not think of itself as a financial market participant. Non-financial counterparties are still counterparties. A hedging arrangement for FX or interest rate exposure can be enough to bring the LEI into view.

A useful way to think about the main company triggers is this:

- MiFIR transaction reporting: an investment firm needs the legal person client’s LEI when reporting trades under MiFID II rules

- EMIR derivatives reporting: legal entities in reportable derivative contracts need LEIs, including counterparties and certain other identified entities

- Issuer identification in FIRDS: issuers of financial instruments traded on venue systems are identified with LEIs in reference data submissions

This is why two companies with the same Irish legal form can have very different outcomes. One might never need an LEI. The other might need one this week because it is moving into a regulated market workflow.

Irish funds and investment structures that may need an LEI

Funds are among the most common LEI users in Ireland. That is no surprise. Irish fund structures sit close to regulated markets, administrators, depositaries, trading counterparties and Central Bank reporting processes.

The exact trigger depends on the structure and the activity. A UCITS, an AIF, a sub-fund, or an investment vehicle used within a wider fund arrangement may need an LEI because it trades instruments, enters derivatives, appears in regulatory filings, or is identified in operational systems tied to reporting. The Central Bank of Ireland’s fund reporting framework and portal-based submissions also sit within this broader reporting environment.

An AIFM may be the reporting party for some purposes, but the underlying fund or compartment can still need its own LEI where the entity itself must be identified. That is why fund launches usually treat LEI registration as an early operational item rather than a last-minute admin task.

Section 110 SPVs and Central Bank reporting in Ireland

Section 110 companies deserve separate attention because they sit at the centre of many Irish structured finance and securitisation arrangements. These entities often require an LEI not because they are “SPVs” in the abstract, but because they enter reporting and transaction frameworks very quickly once active.

The Central Bank of Ireland states that Irish-resident Section 110 companies are obliged to report quarterly data under Section 18 of the Central Bank Act 1971. It also states that the SPV registration notification must be sent no later than five working days after the vehicle enters its first financial transactions. The related SPV data return is due no later than 29 working days from the end-quarter reference date.

That timetable is tight. It leaves little room for sorting out identification details after closing. In practice, the LEI is often part of the setup pack for a new SPV because administrators, arrangers and reporting teams need the entity identified cleanly from the start.

Typical Irish structures where this comes up include:

- securitisation vehicles

- note issuance entities

- receivables financing SPVs

- warehousing vehicles

- repackaging structures

There is also an important nuance for some reporting populations. Where an SPV is already reporting to the Central Bank as an FVC, the separate SPV return may not apply. Even so, that does not mean the LEI is irrelevant. If the vehicle trades instruments, enters derivatives, issues securities or appears in other regulated reporting channels, the LEI can still be required for those purposes.

Can Irish charities and non-profits need an LEI?

Yes, they can.

A charity, foundation, school trust or other non-profit body is not exempt just because its mission is charitable. If it is a legal entity and becomes part of a reportable financial arrangement, an LEI may be required.

This usually arises in treasury rather than day-to-day operations. A charity may invest surplus funds, hold listed debt or structured products, or use a derivative to manage currency or interest rate exposure. Once it enters those channels, banks and investment firms may ask for an LEI in the same way they would ask a company or fund.

The practical lesson is simple: non-profit status does not cancel a reporting-based LEI requirement.

What information is needed for an LEI application in Ireland

The application itself is usually straightforward, but accuracy matters. GLEIF describes the LEI record using reference data that identifies the entity and, where relevant, its ownership relationships.

Most applicants will be asked for core entity information and supporting registry details. That commonly includes the legal name, registered address, entity status, company number or equivalent registration reference, and details of the person submitting the application on the entity’s behalf.

The key data categories are:

- Level 1 data: who the entity is, including its official name and registered address

- Level 2 data: who owns the entity, meaning direct and ultimate parent relationship information where applicable

- Registry details: Companies Registration Office or other official register references

- Authorised contact: the person handling the filing, queries and approval process

An LEI also needs annual renewal to remain active. That point is easy to miss. A lapsed LEI can create trading delays, reporting issues and avoidable back-and-forth with counterparties or administrators.

How to decide whether your Irish entity should apply now

A quick internal check usually brings the answer into focus. Look at what the entity is about to do, not just what it is called in the corporate chart.

Useful questions include:

- Is the entity buying or selling financial instruments through an investment firm?

- Is it entering an FX, interest rate, commodity or other derivative contract?

- Is it issuing securities or appearing as an issuer on a trading venue?

- Is it a Section 110 SPV that has entered its first financial transactions?

- Has a bank, broker, administrator or reporting provider asked for an LEI?

If the answer to any of those is yes, waiting rarely helps. LEI registration is usually easiest when handled before onboarding, before trade execution and before a reporting deadline starts to run.

For Irish organisations, that proactive approach tends to save time, reduce operational friction and keep regulated activity moving without interruption.